How safe is Credit Karma and free credit reports?

Credit Karma provides free credit reports, but how safe is the service and is it safe to rely on for major financial decisions?

Your credit score is like your financial lifeline. It affects your interest rates on loans and mortgages and some companies even use your credit score in their hiring decisions. In other words, for most of us, that score matters. Credit Karma provides it, for free.

That's why staying up to date with your credit score is more important today than it's ever been, especially if you're in the habit of moving around jobs.

Everything is becoming digitized, and new websites are launching all the time. But it can be hard to know if sites and apps like Credit Karma are safe or if they are a scam.

Credit Karma provides a free and easy way of viewing your financial history. I discovered Credit Karma earlier this year, and it has drastically simplified my life.

However, it’s always wise to confirm the company you are using is legitimate and safe before jumping in.

The reality is that you should be paranoid about giving any person or company your social security number. If the wrong people get that info, that can easily lead to identity theft or having your financial accounts drained.

[Note from Steve: This is something that I've personally dealt with, and it's not fun!]

Or they might show up at your house asking for money. And nobody wants that.

Before we dive into talking about whether Credit Karma is safe, let’s first look at why you need to stay up to date with your credit report.

Why Your Credit Score Matters

When you borrow money, companies need a way to figure out if you will pay back the money or not. The best way to do that is to dive into your financial past and see if you have any monsters lurking.

What affects your credit score? According to Experian, these are the top 5 credit score factors:

- Payment history. Payment history is the most important ingredient in credit scoring, and even one missed payment can have a negative impact on your score. Lenders want to be sure that you will pay back your debt, and on time, when they are considering you for new credit. Payment history accounts for 35% of your FICO Score, the credit score used by most lenders.

- Credit utilization. Your credit utilization ratio is calculated by dividing the total revolving credit you are currently using by the total of all your revolving credit limits. This ratio looks at how much of your available credit you're utilizing and can give a snapshot of how reliant you are on non-cash funds. Using more than 30% of your available credit is negative to creditors. Credit utilization accounts for 30% of your FICO® Score.

- Credit mix. People with top credit scores often carry a diverse portfolio of credit accounts. Credit scoring models consider the types of accounts and how many of each you have. Lenders use this credit mix to understand past debt experiences and how you have handled them.

- Hard inquiries. Hard inquiries are recorded in your credit file each time a lender requests your credit report as part of their decision-making process. Hard inquiries remain on your credit file for up to two years and can in some cases have a negative impact on your credit scores.

- Negative information. Late or missed payments, foreclosures, collection accounts, and charge-offs are all examples of negative information that can appear in your credit file. These typically indicate that you have defaulted on a loan in the past and can be red flags for lenders looking to approve you for new credit. The effect negative information has on your credit score depends on your overall credit profile and what type of record it is. These records typically stay in your file for at least seven years, so it's best to avoid any negative infraction if at all possible.

In general, you'll want your credit score to be as high as possible.

But with that said, having a high credit score doesn’t necessarily mean you are great with money or have a strong financial foundation. The primary questions your credit score attempts to answer: “Is this person financially reliable and are they currently overextended?”

If you want to get any kind of loan, whether that is for a home, car, credit card, etc. you want to have as high of a credit score as possible. Rates and credit limits are determined by your credit history and credit score. So it is in your best interest to make sure you stay on top of your financial picture.

If there is incorrect information in your credit report, this could have a negative impact on your credit score. But you can’t fix what you are unaware of. This idea is why it is crucial to view your credit score and credit reports periodically.

It would be a shame to apply for a home mortgage, only to find out you’ve been denied for the loan. You also may find yourself applying for a job, and the prospective company pulls up your credit report.

Don’t be taken off guard! Check your credit score and report.

At the very least, having a stellar credit score ensures that you’ll qualify for the lowest interest rates possible, potentially saving you thousands of dollars in interest payments.

What is Credit Karma?

Credit Karma was created in 2007 to provide consumers with their credit score for free and on-demand.

A summary of what they provide is the following:

- View credit scores from Equifax and TransUnion (using VantageScore 3.0)

- Access Equifax and TransUnion credit reports

- Easily view the accounts you have opened or have closed, with the balances reported on your credit reports

- Provides a way to dispute errors on your credit report

- Easily signup for new credit cards, loans, and insurance policies, which are recommended based on your credit score

- Other features that aren’t as obvious include:

- Viewing an estimated value for your vehicles

- Seeing your “insurance score”, which can be used in calculating your chances in lowering your car insurance rate

- Comparing home loan rates with what you are currently paying

- Get estimated rates and approval estimates on personal loans

- See which credit cards you have a high likelihood in qualifying for

- Free tax filing service

- View and post reviews of credit cards

And one of the best features of Credit Karma? Their service is 100% FREE.

Ever since I started using Credit Karma, I’ve made it a habit in logging in once a month. I love being able to quickly pull up my credit score and see how things have changed over time. This feature is an excellent reason to signup for the service ASAP, as you can see how your credit score changes over your financial history. Each time you pull up your score, it will keep that info in their database that you can access at any point.

As part of our strategy in playing financial catch-up, we plan on continuing to use Credit Karma and feel the service provides incredible value.

I recently closed a few credit card accounts, and I noticed my credit score started going down a few points. I expected this to happen, and I’m relieved that Credit Karma is, in fact, pulling in my real credit report.

Is My Information Safe With Credit Karma?

When you are entering your private information, one vital aspect is how safe your data is in their system.

The great news is that Credit Karma has taken the necessary steps in keeping your personal information safe. They currently have around 85+ million members and are growing at a rapid pace.

The fact is data breaches cost millions of dollars to recover from, and stolen data doesn't make for good business. Credit Karma, just like all financial-based companies, has a vested and financial interest in keeping your information as safe as possible.

Being such a massive company, you know the government is keeping a close eye on how they are using data. They also cover the main things you would expect a major company to do in order to keep things secure:

- They use a DigiCert EV SSL certificate, which is the highest grade authentication available

- 128-bit encryption and they limit who and how your SSN is accessed

- A detailed privacy policy that is certified by TRUSTe

- Credit Karma will not sell your personal information to 3rd parties

- They regularly go to 3rd parties to run security audits

- A bug bounty program that pays people to find vulnerabilities and issues in their system

But even though Credit Karma has top-notch security practices doesn’t mean someone couldn’t get access to your account. That’s why you should ensure you are using a secure password and setting answers to your security questions that people can’t guess the answers to.

If you look at the Credit Karma IOS app, you’ll notice they have 130,000 reviews with an average of 5/5 stars.

Apparently, I’m not the only one who loves Credit Karma!

Credit Karma’s mobile app is fantastic. They make you set a security pin, and on my iPhone, I can enable Face ID to make it fast and straightforward in logging into my account. Clearly, they prioritize security and the amount of effort in making every aspect of their system user-friendly shows when you start using their service.

The bottom line is simple: anything can happen, but Credit Karma has demonstrated a proactive approach to keeping their customer's information as safe as possible.

Just like any other site or service, Credit Karma could come under attack and have their systems compromised, but it’s clear to me that they are very proactive in doing everything they can to avoid that.

How Does Credit Karma Make Money?

It would be a huge red flag if a company was collecting your most personal information, and it was unclear how they made money.

This is not an issue with Credit Karma.

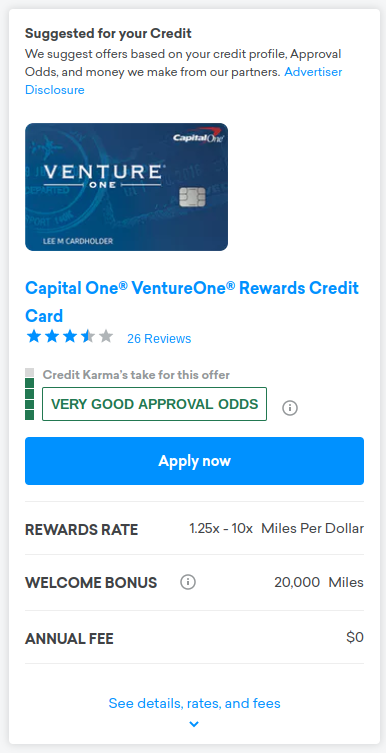

It is true their services and website are 100% free. Like Personal Capital, the way they make money is from the products and services that are recommended once you log in.

For example, the ad to the right was taken straight from Credit Karma.

And, any time someone signs up for a credit card, loan, or service through the Credit Karma website, they earn a hefty commission.

And given how many people use their platform, you know they are probably bringing in big bucks. According to this article, the company had over $500 million in revenue in 2016. The amount of money they bring in is excellent news because you know security has to be a top concern for Credit Karma.

And this confirms they have plenty of money to make sure your data is safe and secure.

But with that said, there are no guarantees that a data breach can’t happen in the future. From what I can tell, I don’t think the risk of this happening with Credit Karma is more significant than any other large company or bank.

Most of the risk lies in someone guessing your password, so make sure you are using a secure password.

The Pain Of Viewing Your Credit Score And Credit Report Before Credit Karma

Before Credit Karma, I was accessing my credit reports for free through AnnualCreditReport.com. This site allows you to view your credit report from the top three companies once a year, for free.

The issue in using AnnualCreditReport.com is that you don’t get access to your credit score, and you can only view your credit reports once per year.

I was also accessing my credit scores through my credit card websites that provided a credit score feature. This process worked okay, but each of them would use a different score, and it was time-consuming pulling each one up. In most cases, they only update your credit score once per month.

I’ve also used other companies in the past that allow you to pull up your credit score and reports, but they often came with significant monthly charges. Before I found Credit Karma, I was seriously contemplating signing up for one of these services.

Credit Karma’s philosophy is that they want to give everyone access to their credit score and reports for free. The more information you have about your financial picture, the more you can make informed decisions about your future. You can use this information in helping put together a livable budget that is sustainable and realistic.

Credit Karma Provides Much More Than Your Credit Score

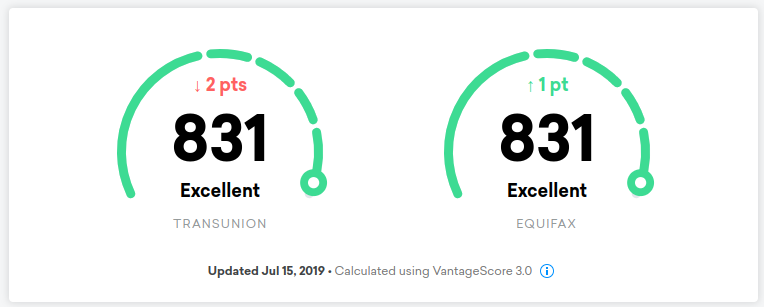

At first, you might think the main benefit of Credit Karma is being able to view your credit score. It might look a little something like below:

But the best feature of Credit Karma is that it also has a credit monitoring service (which is also FREE). Once enabled, you will be notified when there are significant changes to your credit report.

In other words, you immediately get minions working for you that send notifications any time something significant happens on your credit report.

This is a huuuuuge deal.

Let’s say someone manages to get your info and signs up for a new credit card. The only way you would know this happened is by manually viewing your credit report, or getting something in the mail about a new account that you didn’t open.

With Credit Karma, you would get an email (or mobile notification) when that new account shows up on any of your two credit reports. This notification allows you to jump onto this identity fraud ASAP.

A few weeks ago, I was able to test out this feature. I signed up for a new credit card, and a few days later, I ended up getting two emails with the new account that showed up on both of my credit reports in Credit Karma. Ask anyone who has had their identity stolen, and they will scream this is a massive benefit.

Their credit card monitoring feature is another reason you might want to consider opening up a Credit Karama account ASAP. Before, to get this service, you would have to pay a monthly fee. But not anymore!

Are There Alternatives to Credit Karma?

If you have other ways of viewing your credit score and credit reports, don’t feel like you have to use Credit Karma. By now, it’s pretty clear that I think it’s safe to use Credit Karma, but they aren’t the only place where you can get your credit reports for free.

For example, WalletHub, Equifax, and CreditSesame all offer free credit reports.

As long as you are periodically viewing this information to make sure it is accurate, the way you do this doesn’t matter. But there are services out there that charge a fee and don’t provide the benefits Credit Karma does, so it is worth taking a close look to see which is the best option.

Credit Karma is not only safe, but it is more usable than many other “premium” credit card monitoring services I’ve used in the past.

The minimum you should do is view your credit reports for free on AnnualCreditReport.com once per year. You aren’t going to be able to view this information more than once per year, but it is better than doing nothing. And you can access all three credit reports.

The Downside of Credit Karma

Credit Karma is a legitimate and safe company that provides enormous value, especially considering it is free. I couldn’t find any information that inferred that your personal information is at risk using Credit Karma.

But there is one downside to Credit Karma. They only give you access to your credit score and report from two of the three major credit bureaus. You can access TransUnion and Equifax credit reports, but not Experian’s.

In most cases, any changes to your credit will be reported to all three credit agencies. But there is a chance something could only go to one report, and so I would suggest pulling up Experian’s credit report once per year from AnnualCreditReport.com. This plan ensures that if there is some unique discrepancy with that credit report, you can catch the error.

Is this a big issue? Yes and no. It is possible something unique could show up on Experian’s credit report, but in most cases, it will end up showing up in the other reports as well. But it is better to play it safe and cover your bases.

Outside of this one issue, Credit Karma is a fantastic service that is incredibly safe and reliable.

Credit Karma’s Interface Is Optimized To ‘Sell’ You Products

One thing that you should be aware of is that over time the service is tailored to increase the number of people that sign up for credit cards, loans, and other products via their service.

As I mentioned earlier, this is how the company makes sense.

The reason this matters is because if you are the kind of person that makes impulsive decisions and signs up for a new credit card after seeing one ad for it, then spending time on a site which constantly highlights those products might be risky.

While your personal information will be as safe as possible with Credit Karma, that doesn’t mean your financial foundation will be safe if the platform pushes you to take our loans you don’t need. However, if used properly, it can actually make you much more aware of how to improve your finances.

Credit Karma Is A Great Tool In Creating A Strong Financial Foundation

Credit Karma isn’t going to magically improve your credit score or credit history.

But it does provide a fantastic bird’s eye view of your financial picture.

If you are you trying to become credit card debt free, you can use it to ensure your payments end up showing on your credit card reports. Over time, your credit score should increase.

I also found it valuable to see the average age of all my credit card accounts. This info is a crucial data point that is used in generating your credit score and is useful in figuring out if you should close individual credit card accounts. You might not want to close your oldest credit card, for example, as that could drastically reduce the overall average.

You also can see how much debt you have, relative to the amount of credit you have available. Take a look at the image below for an example of how this looks:

All the data I can access from the desktop browser is accessible in their mobile applications. It’s refreshing to see how much info you can access at any point in digging deep into your financial history.

Credit Reports Aren’t Intuitive

If you have ever taken a close look at a credit report, they usually aren’t easy to work through. You might be looking at a long list of accounts, and it is hard to make sense of all of the info.

Credit Karma easily and safely makes the details of your credit report accessible in your account in an incredibly intuitive way.

I’m amazed at the amount of clarity I now have about my credit history. I now look forward to seeing my credit score and credit report! I’ve never been this excited about my credit report in the past. It always felt like a chore. But now I’m passionate about digging deep into the details, and ensuring the information in my credit reports is accurate.

If you are married, make sure that both you and your spouse signup for accounts. There might be some something unique in one of your credit reports. And since each Credit Karma account is free, there hasn’t been a better time to make sure your whole financial house is in order.

Entering your social security number and personal information into a website form can be incredibly scary. Given the history of Credit Karma and the lengths they have gone in securing your data, you can feel confident that your info is safe. But like anything in life, especially on the internet, there are no guarantees, and most of the risk involves the strength of your password, the answers to your security questions, and making sure your email account is locked down.

I highly recommend giving Credit Karma a try. I’m confident my info is safe, and it provides useful information I can access at any time.

This post was originally published on The Money Mix and has been adapted and reused with permission.